SHARE THIS ARTICLE

Contents

- Reclaiming Customer Mindshare in India’s Digital Payments

- UPI Has Evolved from Infrastructure to an Ecosystem Led by Fintechs

- The Business Case for Reimagining UPI

- Dimensions of UPI innovation

- Next Steps for Banks

- Playing to Win

Reclaiming Customer Mindshare in India’s Digital Payments

The Uncomfortable Truth about Customer Ownership

In a recent workshop with the leadership team of a private Indian bank, I posed a simple question:

“You have lakhs of UPI customers transacting on TPAPs using your bank’s accounts. Are you able to meaningfully cross-sell financial products – insurance, investments, credit – to them?”

The answer was telling.

UPI now powers nearly 85% of India’s retail digital payments, yet customer mindshare has shifted decisively from banks to third-party apps (TPAPs). A typical user opens PhonePe, Google Pay, or Paytm 25-30 times a month, but rarely visits their own bank’s app.

The challenge is no longer infrastructure – it’s experience. Banks risk losing relevance unless they reimagine UPI as a product, build differentiated offerings, and anchor usage back into their apps.

UPI Has Evolved from Infrastructure to an Ecosystem Led by Fintechs

When UPI launched, banks viewed it primarily as payment rail infrastructure. Its evolution, however, has been remarkable with continuous product and feature innovation driving an incredible multiplier effect.

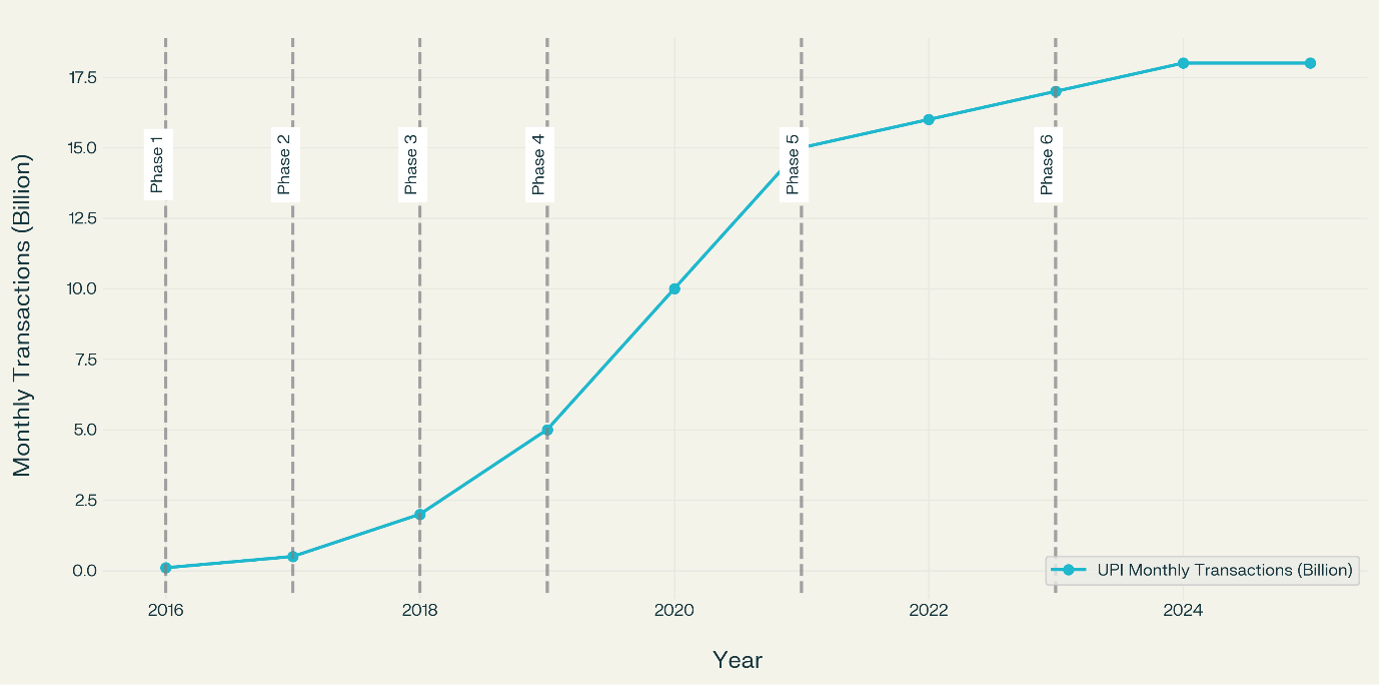

Image 1: UPI’s Evolution and Growth

Today, UPI processes an average of 19 billion transactions monthly. NPCI’s ambition is even bolder: scaling to 1 billion transactions daily (30 billion monthly) with a long-term target of 200 billion monthly transactions within three years1 . As percentage of global real-time payment volume – UPI accounts for nearly 50% and UPI processes more daily transactions than VISA.

Top 5 banks UPI Ecosystem contribution –

| Rank | Bank | Primary UPI Contribution |

| 1 | SBI | Largest payer-side volume (25–27%) |

| 2 | HDFC Bank | ~19% of total UPI volume (payer and payee) |

| 3 | ICICI Bank | ~16% of total UPI volume |

| 4 | Yes Bank | Leading beneficiary bank for merchant payments (≈40%) |

| 5 | Axis Bank | ~10% beneficiary share; growing payer transaction presence |

Over 90 % of this transaction volume flows through the top three TPAPs – PhonePe, Google Pay, and Paytm – dominating market share. PhonePe, G-Pay, Paytm contributes about 49%, 37% and 7% respectively. What started as payment apps have evolved into comprehensive financial service platforms. For example, Cred is launching co-branded credit cards, offering personal loans, and building a complete fintech ecosystem around their payment interface.

The customer mindshare has decisively shifted from banks to non-banking entities, not because banks lack capability, but because they don’t control the customer interface.

The Business Case for Reimagining UPI

Most banks have already invested in a UPI stack to function as issuers of UPI instruments, while many offer PSP services as well. However, this stack is currently being used only for routing and execution. Banks need to develop innovative issuer-PSP solutions to reclaim leadership in payments.

This shift will deliver tangible financial benefits for banks by driving:

- Customer engagement: Retaining customers within your own bank rails directly correlates with higher product penetration and customer lifetime value.

- Cross-selling opportunities: Your most active customers – those conducting 25+ UPI transactions monthly – are prime candidates for insurance, investment products, and credit facilities. Direct access to data on their daily financial behaviour enables more targeted discovery and cross selling.

- PSP fee retention: Every UPI transaction generates a Payment Service Provider fee. While not substantial per transaction (approximately 10 paise), at scale, this represents significant lost revenue that could offset UPI infrastructure costs.

Dimensions of UPI Innovation

Banks have superior customer data, regulatory advantages, and existing relationships – yet they’re losing ground to focused fintech players. Banks must leverage these advantages and innovate in a strategic manner across three dimensions to reclaim customer mindshare.

1. Customer Experience Innovation

As issuers of UPI payment instruments banks can offer innovative onboarding, controls, instruments and rewards to offer customers compelling propositions. Following are some experiences that can help banks drive deeper customer engagement.

- Seamless UPI Onboarding: Like push provisioning for cards, enable customers to set their UPI PIN and link accounts to UPI and merchant apps without leaving the bank app.

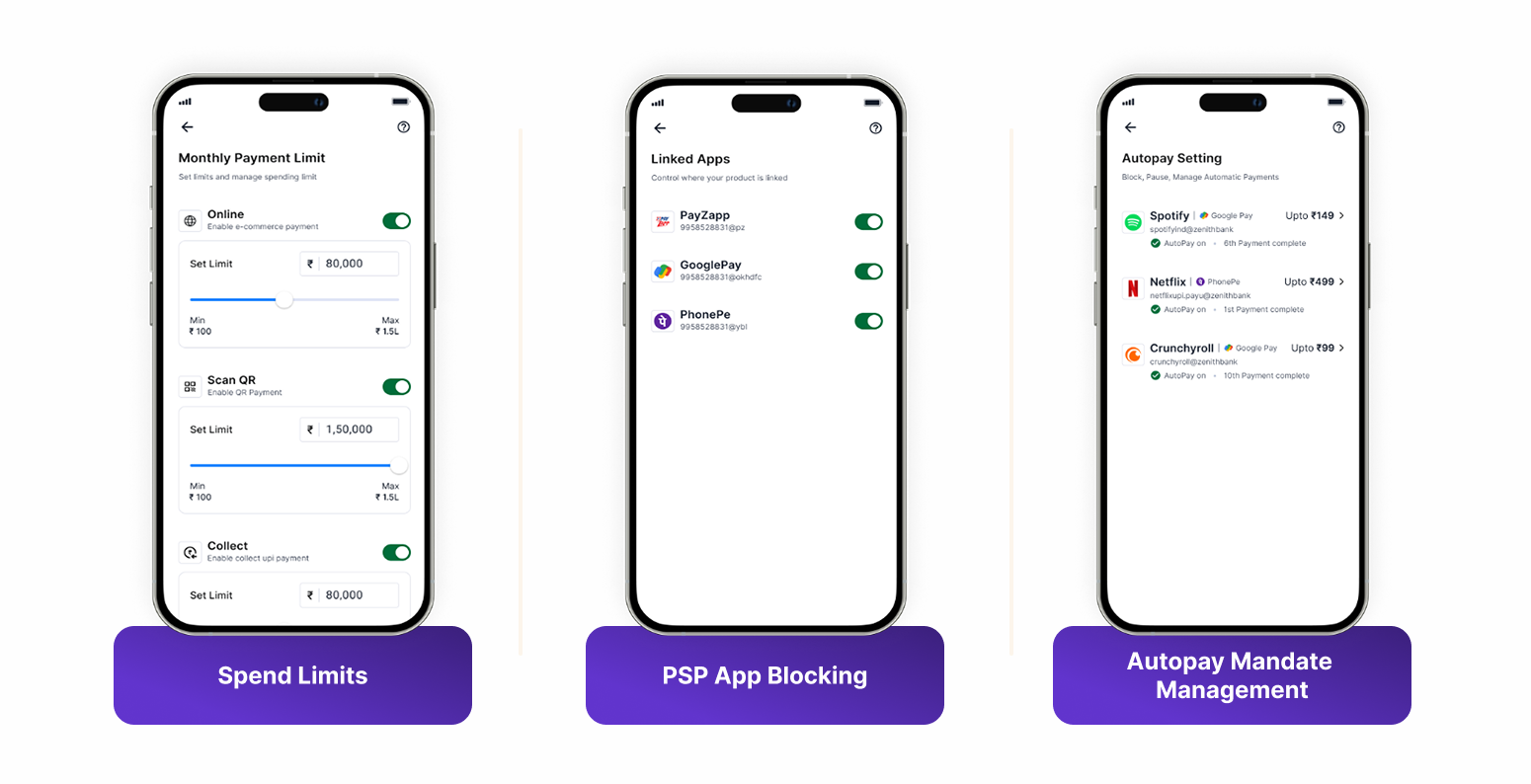

- UPI Transaction Controls: Offer advanced instrument controls, allowing customers to enable/disable UPI apps, set time-based transaction limits, or require additional authentication for high-value collect requests after certain hours.

Image 2: UPI Transaction Controls

- Add-on UPI Experiences: Build niche experiences for families and small businesses, allowing them to delegate payments or create add-on accounts with unified payments tracking and controls.

- Intelligent Rewards Integration: Enable real-time reward point redemption during transactions – imagine completing a ₹100 payment using ₹20 from accumulated reward points and ₹80 from the bank account seamlessly.

- Integrated Lending on UPI: Allow customers to contextually access and activate credit options like BNPL, EMI loans or credit lines while making UPI payments.

- Privacy Protected UPI: Offer protection from fraudulent and unsolicited payment requests and misuse of UPI IDs. Issue one-time use anonymous VPAs on demand to help customers complete UPI payments without revealing their UPI ID.

2. Merchant Acquisition Innovation

With most merchant acquisition being driven by intermediaries, banks can offer innovative onboarding and settlement arrangements, custom payment experiences as well as embedded credit solutions to regain control.

- Current Account Acquisition: Use UPI merchant onboarding as a pathway to comprehensive business banking relationships by offering solutions that help merchants manage payment flows to multiple current accounts via one QR.

- Differentiated Merchant Experience: Offer value-added services like custom QR code solutions, bulk QR printing, EMI integration at point-of-sale, and instant settlement options for compelling merchant value propositions.

- Embedded Credit Solutions: Expand lending to merchants backed by UPI cashflows with integrated lending like merchant cash advance, daily installment loans, etc.

You can view these and other innovative customer and merchant experience use cases in action in our ebook on UPI payment experiences here.

3. Technology Architecture Evolution

Most banks currently rely on single-switch architecture for UPI processing. The opportunity lies in implementing intelligent routing capabilities on top of existing architecture to enable:

- Dual-Switch Strategy: Deploy routers that can dynamically route transactions based on predefined logic; for example, low-value transactions to one switch, salary account-linked transactions to another.

- Advanced Switching Logic: Create rule-based routing for different customer segments, transaction types, or risk profiles.

- Enhanced Processing Capabilities: Build infrastructure that supports complex, real-time decision-making during transaction flow to power advanced UPI offerings to merchants and businesses that deal with high payment volumes.

Next Steps for Banks

Key strategic steps for the bank leadership to reimagine UPI:

Enhancement of customer experience: Invest in customer experience innovation that brings transaction volume back to bank rails. Even capturing 50% of current third-party app usage would dramatically improve cross-selling success rates and customer engagement metrics.

Technology revamp: Evaluate current UPI switching arrangements and assess opportunities for router implementation. This isn’t about replacing existing infrastructure but enhancing it with intelligent capabilities.

Business Model Innovation: Develop new revenue streams from UPI beyond traditional transaction processing. This includes Credit Lines on UPI, family banking, instant rewards, merchant loans based on UPI cashflows, instant EMI, leverage UPI payments trail to underwrite & cross sell digital financial products are just a few possibilities.

Organizational Alignment: Ensure product, technology, and business teams are aligned on UPI as a customer engagement platform, not just payment infrastructure.

Playing to Win

The question isn’t whether banks can compete for dominance in UPI payments, but whether they will choose to do so strategically and aggressively.

The UPI ecosystem will continue expanding – international adoption, enhanced credit integration, and new use cases will drive further growth. With the right approach to payments innovation, banks can play a definitive role in this ecosystem.

The team at Zeta is building UPI solutions that enable banks to compete effectively for payments leadership while maximizing their existing infrastructure investments. If you’re developing a digital payments strategy for your bank and want to explore how to reclaim customer mindshare in UPI, I’d welcome a conversation about what’s possible.

References

-

- Times of India | 1 Billion Transactions per Day for Next 2-3 Years | April 2025